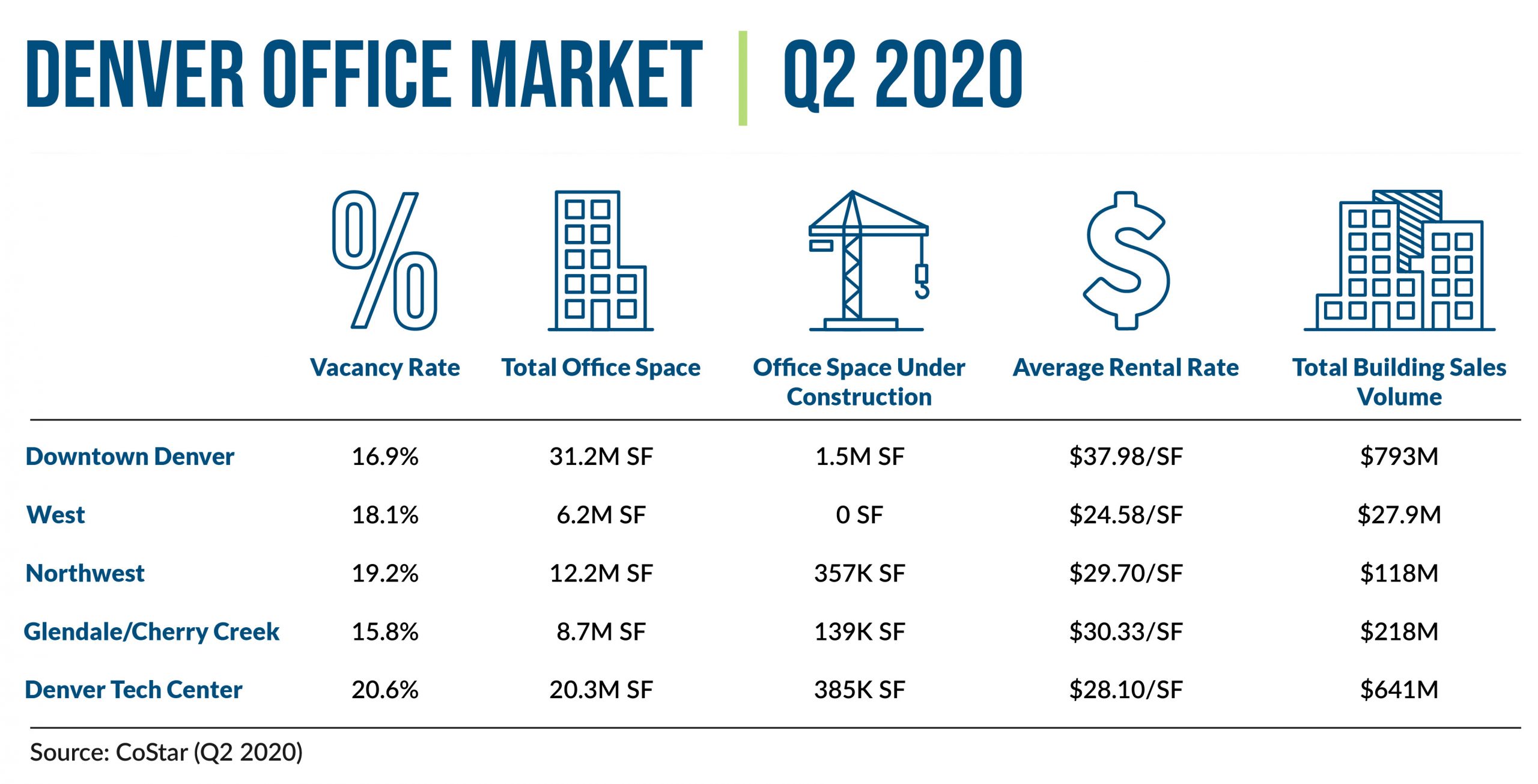

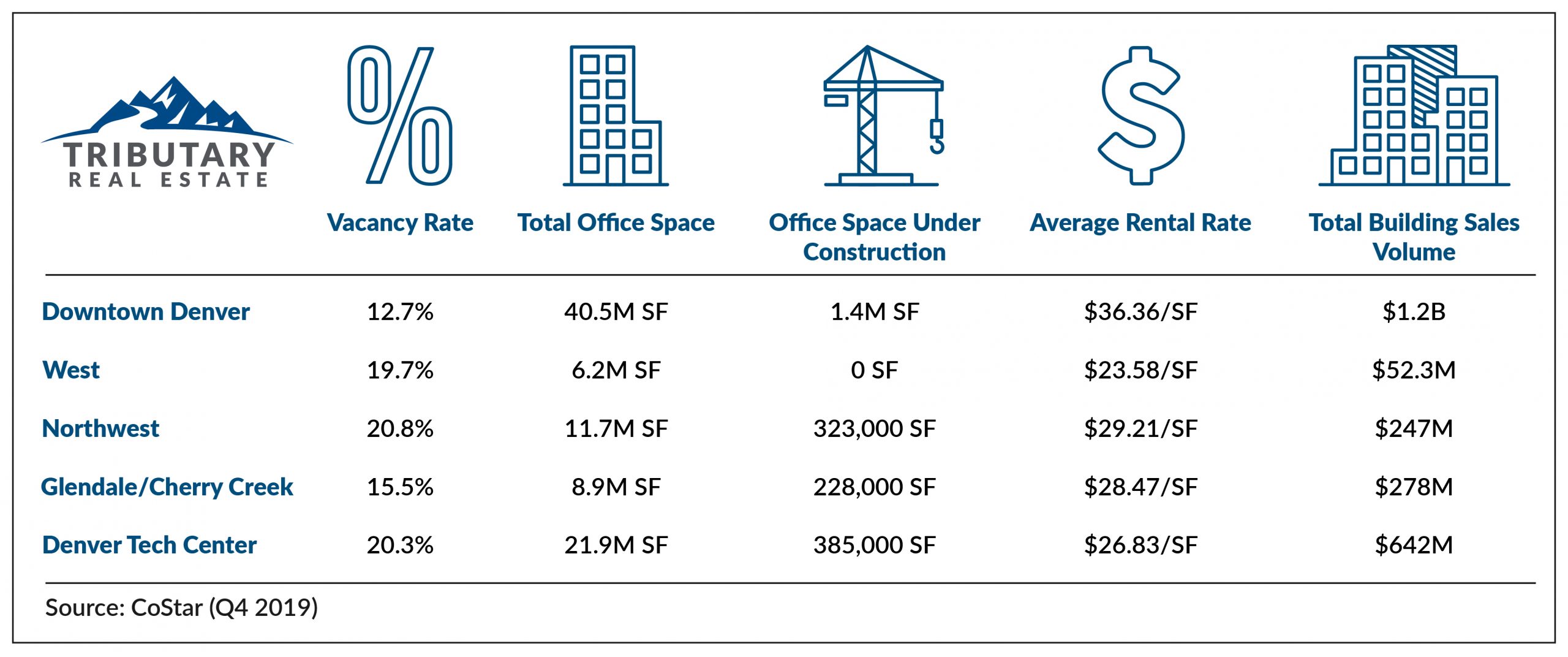

Denver Office Market Update Q2 2020

Denver’s commercial real estate market entered Q2 2020 in a strong position, even as COVID-19 forced the majority of the state to shut down starting in mid-March. While Denver’s office landscape is starting to shift as companies re-evaluate their space needs, there is steady activity across the Denver metro area.

Here are some highlights of Denver’s commercial real estate activity in Q2 2020.

Downtown Denver

- The market continues to shift as 58 new subleases have hit the downtown market since April 1.

- Facebook announced plans to double the size of its office at 1900 16th St.

- Occidental Petroleum Corp. is looking to sublease six floors totaling 130,068 square feet at 1099 18th St.

- Dispatch Health raised $136M in Series C funding.

- A parking lot at 1300 Cherokee St. in the Golden Triangle sold for $6.7 million.

West Denver

- Bancroft acquired Union Terrace Building for $11,327,200 or $132.62/sf. The building was 86% leased at the time of the sale.

- Tap Rock Resources leased 23,000 sf at 523 Park Point Dr. in Genesee.

- Golden View Classical Academy acquired a 54,396-square-foot building at 601 Corporate Circle for $7,783,400 or $143.09/sf.

- Next Level Sports Performance acquired a 10,875-square-foot building at 4670 Table Mountain Dr. for $2,325,000 or $213.79/sf.

Northwest Denver

- Rowdy Mermaid, a kombucha startup in Boulder, raised $3.5M.

- Crocs opened its new headquarters at ATRIA in Broomfield.

- Office Evolution, a Louisville-based coworking franchisor, opened its 15thColorado location in Northglenn.

Colorado Blvd/Glendale/Cherry Creek

- The Citadel building in Cherry Creek sold for $33M.

- Former Inn at Cherry Creek announced plans to reopen next year as The Clayton.

- BMC Investments broke ground on a 6-story building in Cherry Creek, anchored by Equinox fitness club.

Denver Tech Center

- Vectra Bank submitted plans to build a nine-story HQ within Belleview Station.

- Boom Supersonic, a startup looking to build commercial supersonic jets, raised $3 million.

- The landlord of the six-story Tuscany Plaza in Greenwood Village sued Red Robin for unpaid rent.

{kind=link}